To effectively elucidate the causal relationships between various economic processes, it is vital to delineate the evolution of their patterns. For example, recent developments in interest rates highlight the potential correlations among different rates. The onset of global trade tensions, initiated by former President Trump’s policies, has prompted notable adjustments, including reductions in rates by various countries due to decisions made by international institutions such as the European Central Bank (ECB) (see https://www.lesechos.fr/finance-marches/marches-financiers/la-bce-choisit-de-baisser-ses-taux-face-a-lincertitude-economique-2160609). Additionally, the Federal Reserve (FED) is facing pressure to lower its rates in response to these external influences (https://www.marketwatch.com/story/trump-is-furious-that-fed-wont-cut-interest-rates-like-ecb-heres-why-powell-wont-budge-162dfdaa).

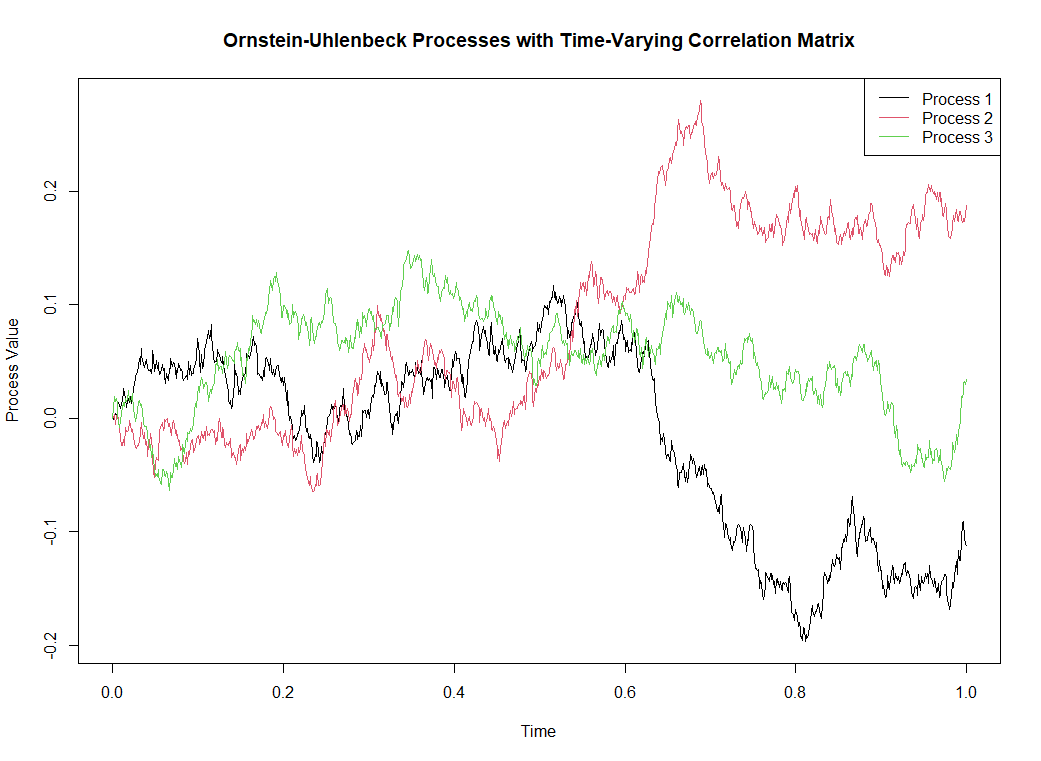

A straightforward approach to modeling the evolution of interest rates is through stochastic processes, such as the Ornstein-Uhlenbeck process. Although potential negative rates present a challenge, our focus will be on further exploring multivariate scenarios. Should it be imperative to avoid negative rates, the Heston-White model presents a viable alternative. For a thorough examination of interest rate modeling, refer to the comprehensive work of Damiano Brigo and Fabio Mercurio.

In the following, we are interested in the stochastic differential equation of the form

where the second term shall be generalized. But what generalization?

We thus introduce the vector stochastic processof dimension

(

is a

matrix describing the trends of the vector stochastic processes.

In other posts of the present blog, the following equation was proposed.

whereis a function, assumed to be at least continuous on

(or

is assumed to be some positive number. Finally,

is a vector of standard Wiener processes. The function

First, we note that this equation gives

This means that") defining some metric of integration. Since

and

are the only forms which we consider in this equation, then we heuristically we:

where the's are Borealian functions of

and we ignore the terms of the form

with

, and

with

. Considering now the fact that

could be set to zero. Thus we have:

Using again the fact that, we should have

where the's are other Borelian functions but only depending on

This (vector) equation turns out to be the most possible general stochastic differential equation related to the functionis a vector of dimension

is a matrix of dimension

If the processes only have dependencies in their stochastic terms, we shall setto be a vector only depending on time

, so that the final quation of interest is given by:

We integrate this equation by setting:

The Itô's lemma gives:

Therefore, integration of this process finally leads to:

Now, we note that the only random term is the third one, which has zero expected value. Therefore, we have

In words,. It shall be interesting to see in which circumstances the matrix

and vector

may lead to a non-explosive process.